I figured for my first real post, it's probably best to start at the beginning. I have been gainfully employed since May of 2000, luckily all this time at the same company. My early investing days were nothing special. I participated in not only our employee stock purchase program, but as well as in our 401K program. Long story short, we eventually went private to reorganize our company, so we got compensated for our public stocks, which was not much to write home about for me. Throughout this I continued to put money away into my 401K however.

As the years went on and I became more and more interested in the market and strategies, especially since 2000 to current is being called the worst 10+yrs in the history of the market, I was looking for a way to generate returns without having to "guess" on which stocks would give you a capital gain. Almost by accident I had an account (I have 3 currently. 401K, "Fun Money" and my "Self Run 401k" - which is my dividend portfolio) that just happen to have MCD and PEP in it. I kept noticing every quarter that these stocks would not only give me back some money, but every year or so, the amount seemed to go up. Not being a finance major, or ever really being taught on economics, I went to research why I was getting this money back. Low and behold, the word "dividend" was something I became very interested in and read up on it as much as I could.

This was around 2008 and I decided to create my "Fun Money" account. I was still throwing as much money as I could into my 401K and pretty much that was it. I decided to explore these dividend stocks a little more and create the account thinking I'll see what kind of returns I can create with it. Even through the rough market times of 2008 until now, the account consistently was throwing off increasing dividends (and since I got in at some of the lows of 2008, some nice capital appreciation as well). I thought to myself, "Wow, there is something here behind this strategy."

So after playing with the "Fun Money" account for 3 years, I decided to change my retirement strategy as well. In Jan of this year, I decided to cut my 401K contributions to the amount where the company matches it fully and take the rest and run my own "401K" account. There were a couple of reasons I felt this was a good move.

1. Late last year, my normal 401K account had grown luckily to over 6 figures. I am very lucky/fortunate in finding the job I have, I realize this every day. That, along with my desire to have financial stability, has lead me to be a very prudent saver. The amount in there at such a relatively young age, at least in regards to investing, had given me a sense of security so to speak to explore other options.

2. One of the biggest flaws I see in the 401K is the minimum age before you can touch the money. Say you are fortunate to retire at 45, or even 50. Well guess what? You can't touch the 401K without paying "penalties" before 59. Personally I'm hoping to retire before 59. So this presented a problem, how would I support myself before 59 if I'm retired? I needed a way to "fill in that gap" so to speak. And dividends spoke to that need loud and clear. (Yes I realize on the flip side that dividends are taxed, etc, etc, to me the trade off of having the money when I want it without penalty and being able to do with it what I want is worth it to me). On top of this you have to actually sell the mutual funds in your 401K to get your money, yes some mutual funds pay distributions, but they can be inconsistent and can go up and down themselves. So eventually, your 401K goes from it's full amount on the day you retire to zero (well in theory at least). To me it seems there has to be a better option than that.

3. It's fun, it's really a hobby to me now. This stemmed from my "Fun Money" account. Checking the different company links when you know the general time of announcement dates, seeing the dividends increase year after year, watching your personal dividend paybacks going up quarter after quarter in the numerous spreadsheets. To me it's really exciting and an enjoyable way to pass some time.

4. It's not only setting up me, but my children and their children for future generations. I'll go into this in another post, but with dividends, it's all about having time to let the dividends grow. Eventually my plan is to roll my dividends into my estate plan, so when the reaper gets me, I have set up parameters to where my children (two girls), will not be able to sell any of the stocks I acquired (unless certain parameters are hit where a stock is tanking), but rather will continue on receiving the dividends I had established. (And hopefully in 50+ years, some of those might be throwing off 30-40% annually for them)

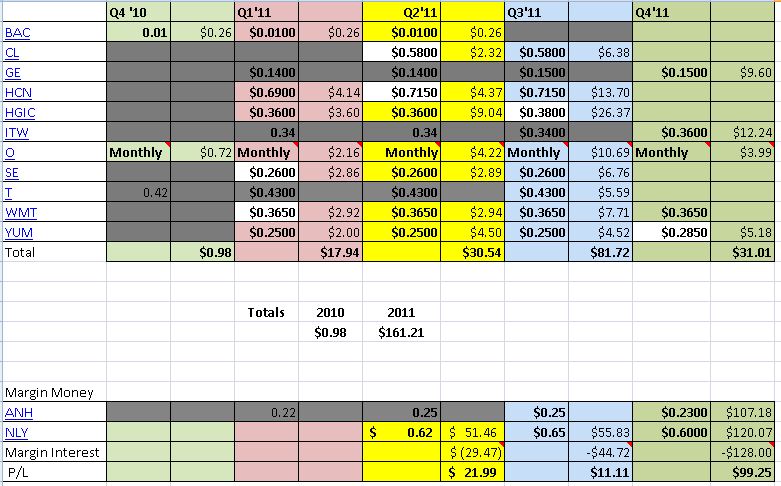

So that's my story for now. Currently, like I said, I have 3 accounts. My normal 401K, my "Fun Money" account, and the "Self Run 401K" account that I started in Jan 2011, that this blog will focus on. I plan to very transparent with the amounts I have invested, returns, etc. Also if you have any questions don't hesitate to ask. As the disclaimer states, I'm no trader, financial adviser,etc. Just a normal guy who has done a lot of reading on dividend stocks and who really likes this strategy to investing. I'll leave you with my current returns, and in the next post go over the different stocks I have right now, why I chose them, and the margin strategy I am currently engaged in as well.

No comments:

Post a Comment